View the recorded session discussing this article’s topics in detail:

Want a guided tour of IncomeConductor?

Set up a personalized demo at a time that works for you.

Does this sounds familiar? You spend 20 years building a relationship with a client couple. You go to their family events, celebrate their birthdays, sends gifts, include the husband in your golf outings, etc. Maybe you even reached out to the kids in order to secure generational wealth transfer.

But what you may not have done is forge a bond with the wife as an individual, perhaps defaulting to the husband as the decision maker and even primary contact.

There is a tremendous transfer of wealth taking place in the U.S. and surprisingly it is not necessarily to the children of retirees. Instead, it is to surviving spouses, who are predominantly women. What should be alarming to financial advisors is that 80-90% of these surviving spouses are changing advisors[1], regardless of the length of the relationship with their current advisor as a couple.

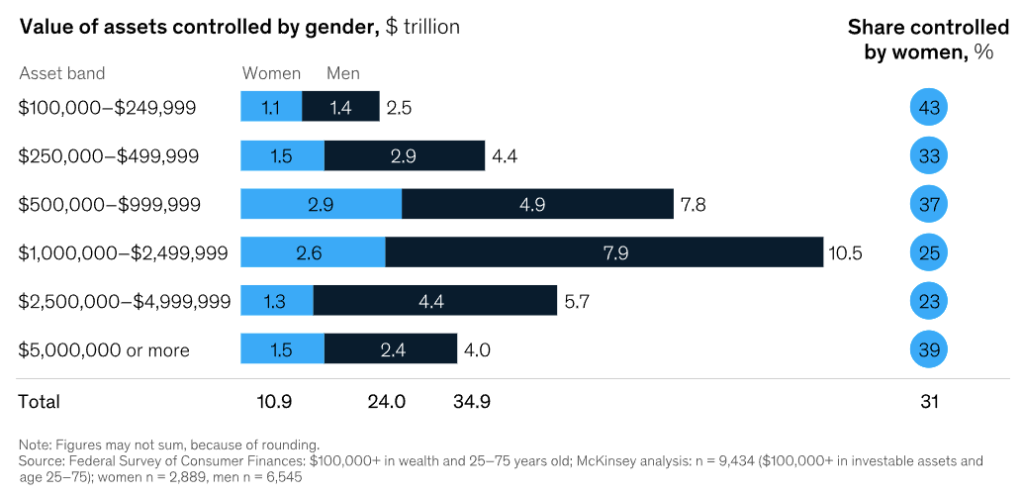

Historically, according to McKinsey & Associates[2], 66% of financial decision making was done by men. However, of the 70% of the wealth in the U.S. controlled by Boomers, 43% of this wealth will be controlled by women by 2030. As a result, the majority of financial decision making will gradually transition to predominantly women, especially within the “Mass Affluent”.

Why are surviving spouses looking for different advisors? From our research there are three primary reasons:

- The spouse was never engaged in the retirement income planning process

- The children of the surviving spouse influenced their parents decision to change advisors

- The surviving spouse felt there was never a “Plan” in place that addressed her needs

According to Kiplinger[3], 80% of men die married, while 80% of women die single.

Many financial planning tools that analyze wealth transfer focus on generational transition of the the “last to die’s” wealth and totally ignore the first transfer to the surviving spouse. Kiplinger also reported that most women prefer female advisors and yet, less than 20% of advisors in the U.S. are female.

With trillions of dollars forecasted to transfer to surviving spouses over the next decade, advisors need to step up their financial planning practices to avoid losing significant amounts of their AUM.

In the session linked above this article, Phil Lubinski, CFP shares his personal experiences and methods he developed to successfully retain not only the surviving spouse as a client, but ultimately their children as well. He highlights case studies that clearly demonstrate how IncomeConductor can help you address the challenges that surviving spouses face including unique tax planning issues.

Register now to attend live. Once the session has passed, the recording will be linked above.

Want a guided tour of IncomeConductor?

Set up a personalized demo at a time that works for you.